SBIR Reauthorization Status: America's Seed Fund Lives to Fight Another Day

After five months in limbo — the longest shutdown in their 43-year history — the SBIR and STTR programs are coming back from the dead. On February 25, Sens. Joni Ernst (R-IA) and Ed Markey (D-MA) announced a bipartisan compromise bill, the Small Business Innovation and Economic Security Act, reauthorizing the programs through September 2031. The Senate hotlined the bill and passed it unanimously on March 3. The House followed on March 17, 345-41. The bill now goes to the president's desk, ending a standoff that froze new solicitations and awards across all participating federal agencies since October 1, 2025.

The breakthrough reportedly came after Pentagon officials threatened to redirect funding if the program wasn't quickly reauthorized, which served as an effective reminder that the Department of War is its largest customer. Space Force acquisition officials had begun publicly sounding the alarm, with Space RCO director Kelly Hammett revealing that contracts for satellite sensing payloads — "sensors that tell you something is tracking you" — were sitting on ice, fully evaluated and ready to award, waiting on Congress.

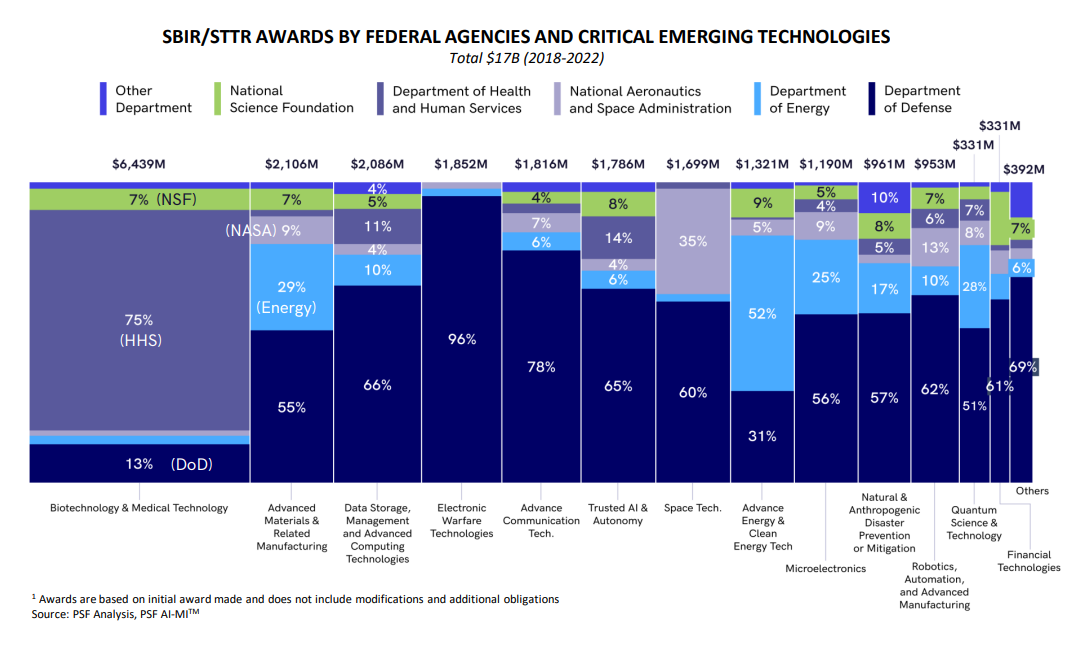

SBIR participating agencies

What's in the Deal

The compromise threads the needle between Ernst's aggressive reform push and the Markey-led effort to protect the ecosystem that already existed. The compromise gives both sides enough to claim a win, though Markey’s office certainly did the heavier lifting in the negotiations that got the bill across the line.

The big fight was over lifetime caps. Ernst's original INNOVATE Act proposed a $75M lifetime ceiling on SBIR awards per company. This was the most controversial provision and the one that Markey refused to accept. He argued it would punish companies with legitimate track records.

The lifetime cap has been removed. Instead, agencies must now cap the number of proposals a single company can submit per fiscal year, per solicitation, or per topic. Agency SBIR directors retain the flexibility to waive these limits for time-sensitive or urgent technology needs, but waiver authority is capped at 5% of topics in any given fiscal year.

The bill also creates Strategic Breakthrough Awards: a new post-Phase II pathway enabling agencies to make jumbo awards up to $30M with matching private or non-SBIR government funding, capped at 48 months. Much like STRATFI/TACFI, this calls for co-investment from the private sector, imposing market discipline at a critical scaling phase – and putting the onus on companies to attract matching capital and prove they’re building something someone other than a government grant officer believes in.

Tighter due diligence on foreign ownership and influence was the easy part of the process, attracting zero opposition from either side. New data collection requirements were similarly uncontroversial, though they may end up mattering more than folks are pricing in. Agencies now have to track Phase III transitions, direct-to-Phase II awards, and subcontracting data, which they were not doing well before. This introduces a new level of rigor that the program never previously required.

Critically, the bill lets agencies roll unspent FY2026 SBIR/STTR funds into FY2027, a necessary patch so none of the money evaporates after five months of dead air.

The five-year reauthorization through September 30, 2031 puts the next sunset in an off-election year. A small mercy, and most welcome bit of legislative common sense!

A Tough Convo on So-Called “SBIR Mills”

The entire lapse largely boiled down to one single question: what do you do with the companies that have co-opted America's Seed Fund into a permanent revenue stream?

The SBIR program was designed as seed capital: early money to help small businesses prove out a technology and get to market. But a handful of firms have built entire business models around winning SBIR awards in perpetuity (known pejoratively in the industry as “SBIR mills.”)

The mills employ professional proposal writing teams and respond to dozens or hundreds of specific government topic areas per year. They treat the program less as seed capital and more as ARR (annual recurring revenue). To give two of the most egregious examples: Physical Sciences Inc. has received 1,728 SBIR/STTR awards worth $650M since 1983, which is more SBIR dollars than all small businesses in 26 states combined. Triton Systems has won 906 awards totaling $365M.

A 2024 GAO report found that these "multi-award winners" represent less than 1% of SBIR participants but soak up over 10% of Phase II dollars. The top 22 firms alone secured 17% of all DoD Phase II funding between 2011 and 2020. The cherry on top was that these mills produced fewer patents and weaker commercialization metrics than their peers — meaning the companies consuming the most SBIR money are, by the government's own measurement, the worst at turning it into anything useful.

Ernst wanted to "clean those bastards out," as one commentator said. The venture-backed startup community largely agreed. There’s deep resentment that entrenched R&D houses whose core competency is grant writing (rather than scaling technology) crowd out newcomers who could actually use the capital to build products and hire people.

This frustration is entirely legitimate. When less than 1% of participants absorb that much funding while producing the weakest commercialization results in the program, something needs fixing. But a hard lifetime cap was never the right fix. The lifetime caps proposed in INNOVATE would have likely prompted the largest mills to break apart into dozens of smaller entities, each with a fresh allocation. This would mean more competition for small businesses, not a better fighting chance.

The better answer, in our view, is Open Topic solicitations. Mills thrive on specific topics because their whole business model is professional proposal writing teams responding to defined government requirements. They don't make products of their own, so they sit out open topics, where a company has to bring a genuine capability to the table. Markey pushed for stronger Open Topic language in the bill. Ernst removed it—which, if you're keeping score, undercut her own stated goal of limiting mills.

Why SBIR Can’t Be Replaced

We are not neutral parties here. Let’s be clear on that. As a Platform that has helped its clients win over $600M in SBIR awards, we’ve earned credibility here (we’d like to think). We have a distinct point of view on these programs, and that view is that the program’s loudest critics have gotten it wrong.

Yes, SBIR has a mills problem. Yes, commercialization rates are so-so (only ~16% of companies transition beyond Phase II, per a Naval Postgraduate School study). Yes, the valley between R&D funding and programs of record remains brutally real.

But none of this negates what the program does. America’s Seed Fund, as NSF has called it, has delivered over $77B in R&D funding to more than 33,000 small businesses over four decades. The NVCA estimates every federal dollar spent through these programs leverages more than $15 in VC.

Qualcomm, believe it or not, was once a small business whose first outside funding was an SBIR grant. The same goes for Symantec, iRobot, Illumina, and Biogen. Anduril parlayed Phase I and II SBIRs into $4B+ in government contracts and $7B in private investment. Starfish Space went from a $50K SBIR to $50M+ in VC and $10s of millions in Phase III contracts.

In our view, there are three reasons you can’t entirely replace SBIR with private capital:

It funds what VCs (initially) won't touch. VC optimizes for 10x returns within 5-10 years. This venture math filters out deep tech companies with long development timelines, government-specific use cases, or markets too illegible for early-stage underwriting. SBIR helps fill the gap between "interesting science" and "investable company" that private markets have been known to ignore. As Maj. Gen. Stephen Purdy, the Space Force's acting acquisition head, said: "venture capital and private equity only go so far. They want to see government interest.”

Non-dilutive capital at the most dilutive stage. SBIR provides non-dilutive capital at the stage where equity financing is most punishing. A $150K Phase I or $1.2M Phase II doesn't sound like much until you consider that pre-revenue deep tech founders are selling 20-30% of their company per round. SBIR lets founding teams de-risk technology, build prototypes, and demonstrate government demand before they negotiate with investors. Founders keep more of their companies. Investors get in at a later, better-understood risk profile.

The award itself is a demand signal. A SBIR from AFWERX or SpaceWERX tells VCs that the government has a real need for this technology and is willing to put money behind it. Defense-focused firms like Shield Capital explicitly look for SBIR traction as a proxy for product-market fit. If you kill the program, you sever the link between government problem sets and the private capital that funds solutions to them.

Source: Public Spend Forum June 2023 SBIR/STTR report.

What Comes Next

The bill goes to the Resolute Desk for the President’s signature. Once signed, agencies will need to stand up new solicitation timelines quickly. Five months of dead air means a backlog of topics, unfunded proposals, and startups that burned through runway while waiting on Washington. The FY2026 rollover provision will help, but it won't give anyone those months back.

Whether the reforms truly disincentivize the worst behavior is an open question, but consider us optimists on this count. Proposal limits are a softer instrument than a hard cap, and determined mills will try to adapt, but more stringent data collection and Phase III tracking will be a powerful deterrent. If agencies are finally forced to measure and report transition rates, the political pressure to fund companies that actually commercialize will build on its own. As CSIS noted, the inability to quantify SBIR-to-production conversions is what allows critics to cast doubt on the program's value in the first place.

In our view, Markey deserves more credit than he'll get. He fought for a permanent reauthorization and a doubling of the budget. He didn't get either. But he killed the lifetime cap, preserved the STTR program, secured the FY2026 funding rollover, and pushed for Open Topic reforms that — even though they were stripped from the final bill — pointed at the right structural fix.

For all of the founders we work with – the ones building satellites, robots, reactors, autonomous vessels, AI tools, and hypersonic propulsion – this reauthorization can’t come soon enough. Every month the program was dark was a month without new solicitations, without new demand signals, and without the non-dilutive capital that makes the whole flywheel turn.

America’s Seed Fund isn’t perfect, but to paraphrase Churchill, it’s the worst form of innovation funding…except for all of the others.

Solicitations are set to come back ASAP. If you’re a startup or small business with technology that our government needs, the window to prepare is now – not after the topics drop. At SBIR Advisors, we’ve helped our clients win over $600M in awards. We’ve got a handful of open slots left for the rest of 2026 – if you want to be ready when agencies start moving again.